The 6 Biggest Accounting Risks for Cannabis Businesses

Most cannabis operators don’t have an accounting problem — they have a “prove it” problem

Most state-licensed cannabis operators I talk to can produce a P&L and a balance sheet.

That’s not the hard part.

The hard part is that cannabis is one of the few industries where you can be fully compliant with state law and still face punishing federal tax treatment, banking friction, and heightened scrutiny from almost everyone who touches your financials—lenders, investors, buyers, and yes, the IRS.

So “good” cannabis accounting isn’t just clean books. It’s defensible positions: on federal tax, on what goes into inventory and cost of goods sold (COGS), on cash controls, and on whether your financial activity matches your licensed activity. In other words, you’re not just closing the month, you’re building a file that can survive questions later.

If you want a deeper look at how we support cannabis operators across compliance, reporting, and tax-aware accounting, see our

cannabis accounting and finance services.

280E is the cash-flow killer — you need to model it like a tax, not a surprise

IRC Section 280E is the headline risk for cannabis accounting for one reason: it can turn a “profitable” business into a cash-starved one.

In plain English, 280E says that if you’re in the business of “trafficking” a Schedule I or II controlled substance (marijuana is still treated that way federally), you can’t deduct ordinary business expenses on your federal return. That means costs that feel fundamental:

rent, payroll, marketing, admin, insurance, software, professional fees—may not reduce federal taxable income the way they do in every other industry.

The result is brutal but predictable: effective tax rates can spike because your taxable income can look nothing like your book income. I’ve seen operators budget for taxes the way a normal retail business would and then get hit with estimated payment requirements that feel disconnected from reality, because the rules don’t match their intuition.

This is where FP&A earns its keep. You need an 280E-aware tax cash forecast that models estimated payments, seasonality, and sensitivity, especially margin compression. If gross margin dips three points because wholesale prices soften or yields come in light, your cash tax burden might not dip with it. You’ve got to know that before it happens, not after the quarter closes. For many operators, that starts with a 13-week cash flow model that makes tax timing and liquidity constraints impossible to ignore.

One more thing I push leaders to internalize: month-end close needs a 280E lens. Otherwise, you’ll confuse accounting profit with usable cash—and in cannabis, that confusion gets expensive fast.

COGS is where cannabis tax strategy actually lives — but the rules are tighter than most people think

280E blocks deductions—but it doesn’t change the concept of gross income. That’s why COGS matters disproportionately in cannabis.

Your tax outcome often comes down to a single practical question: what costs are legitimately included in inventory/COGS, and what costs must stay in nondeductible operating expense? Get it wrong and you can create two different kinds of pain:

- Internally, you might overstate margin and make bad decisions—pricing, hiring, expansion—based on a profitability picture that isn’t real.

- Externally, you might understate taxable income and invite IRS scrutiny, penalties, and back taxes that hammer cash flow.

When people hear “inventory capitalization,” they tend to think it’s a year-end tax adjustment someone else will handle. That mindset doesn’t work here.

Inventory capitalization just means this: certain costs that are connected to producing or acquiring inventory get “stored” on the balance sheet in inventory and then flow through COGS when the product sells. Costs that aren’t properly part of inventory stay as operating expenses—and under 280E, those operating expenses may not help you on federal taxes at all.

The key is that cannabis businesses don’t get to freestyle this. The IRS has specifically addressed inventory-costing rules for marijuana businesses, and their training materials have historically flagged inventory and Section 471 (inventory accounting rules) as central audit focus areas. If your “method” is basically “we’ll see what the preparer does,” you’re building on sand.

What you want instead is a

documented, repeatable methodology

that you run monthly—how you classify costs, how you allocate shared labor, how you treat overhead, and how you handle variances. Not a one-time scramble in March to reverse-engineer a story.

Inventory accounting is unusually sensitive — because you’re reconciling reality, the GL, and seed-to-sale

In most industries, inventory is a technical accounting area.

In cannabis, it’s also an operational and compliance area—which is why it breaks so often.

The risk isn’t just valuation. It’s everything that happens between “we grew it or bought it” and “we sold it”: **shrinkage, waste, spoilage, destruction events, transfers between facilities, repackaging, remediation, write-downs**. Each of those events needs to be reflected in quantities and value, and each one needs an audit trail.

The control stack I like to see isn’t complicated—but it is disciplined: physical counts on a real cadence, variance thresholds that trigger investigation, clear approval for write-offs, and documentation that explains *why* the adjustment exists. If you’re doing adjustments because “that’s what the system says,” you’re one question away from not being able to support your own numbers.

Then there’s the reconciliation problem that’s uniquely cannabis. Your inventory records usually need to tie out across three places:

- Your seed-to-sale / compliance system (the state’s view of your inventory)

- Your POS/ERP or inventory tool (the operational view)

- Your general ledger (GL) (the accounting/tax view)

When those don’t match, it’s not just a messy close. You can end up with tax issues (because COGS is wrong), audit issues (because support doesn’t tie), and licensing issues (because compliance records don’t reflect reality). I’ve seen operators treat that mismatch like an annoying systems issue—until someone external starts asking for tie-outs and the room gets quiet.

Cash handling and banking: if you’re cash-heavy, your controls need to be overbuilt on purpose

Even in 2026, many cannabis businesses still operate with limited banking access—so they carry more cash than a typical retailer would ever tolerate.

FinCEN guidance has made it possible for banks to serve marijuana-related businesses with heavy due diligence and reporting, but “possible” isn’t the same as “easy.” And even when you do have banking, cash volume often stays higher than normal—because of customer behavior, vendor constraints, or the friction of moving money.

That reality changes what “good controls” look like. If you’re cash-heavy, your controls have to be overbuilt on purpose: daily cash reconciliations, deposit logs that tie to actual deposits, vault counts, dual custody, segregation of duties, and tight documentation retention. If refunds, voids, tips, or cash paid-outs aren’t supported cleanly, you’re effectively asking your financials to be questioned.

This is also where

accounting meets diligence. Lenders and investors don’t give cannabis operators the benefit of the doubt on cash. Strong controls reduce the “assume the worst” discount that shows up in underwriting, valuation conversations, and audit scopes.

Better cash documentation makes your month-end faster. When cash is sloppy, every account becomes a mystery account.

Entity structure and related parties can help — or backfire if it’s not a real business separation

A common strategy in cannabis is to separate activities: a plant-touching entity for licensed operations, and separate entities for management services, real estate, IP, staffing, or equipment.

Sometimes that structure is legitimate and helpful.

Sometimes it’s a tax strategy in search of substance—which is where it gets dangerous.

The big misconception is that creating multiple entities automatically improves the tax outcome. It doesn’t. The question the IRS cares about is whether these are truly separate trades or businesses with real economics, real operations, and real records. There are cases (CHAMP is the one everyone cites) that show a separate lawful trade or business can matter—but weak structures can collapse fast under scrutiny.

“Defensible” separation looks like boring, unsexy execution: intercompany agreements that match reality, clear service descriptions, invoices that tie to deliverables, time tracking or cost allocation that isn’t made up after the fact, and clean eliminations/consolidation workpapers so your reporting isn’t double-counting activity.

From an FP&A standpoint, intercompany setups also change how you should read the business. They change margin, cash movement, and tax forecasting. If you only model one entity’s P&L, you’ll miss where the cash is actually going—and you’ll be shocked later when a “profitable” entity can’t make its tax payments.

Indirect taxes and payroll aren’t background noise — they’re liabilities that compound fast

Cannabis operators often focus so hard on 280E that they underweight the taxes that can quietly compound into a real problem: sales tax, excise tax, and local cannabis taxes.

Depending on your state and municipality, you may have multiple layers assessed at different stages—cultivation, transfer, wholesale, retail—with different filing frequencies and definitions. That complexity creates a simple accounting requirement: your chart of accounts has to cleanly separate revenue from pass-through taxes and track liabilities by agency. Otherwise you’ll end up with “phantom margin”—a P&L that looks strong because taxes collected from customers are sitting in income instead of a liability account.

Payroll is the other sleeper issue. In most businesses, payroll is a massive deduction that lowers taxable income.

In cannabis, payroll tied to trafficking may not behave like you expect under 280E—which affects budgeting and tax forecasting. I’ve also seen employers assume normal federal treatment around credits and incentives, only to learn that cannabis doesn’t get to play by normal rules.

The fix isn’t glamorous: build a month-end compliance cadence. Reconcile tax filings to the GL monthly, not quarterly. If you wait, these liabilities don’t just “show up”—they stack, and they hit cash at the worst possible time.

We're Trusted by Growing Cannabis Businesses

How to prioritize your cannabis accounting build-out

If you try to fix everything at once in cannabis finance, you’ll get stuck. The better move is sequencing—because the early decisions drive the later ones.

Here’s the order I’d prioritize:

- 280E position + tax cash forecasting

- COGS / inventory capitalization methodology

- Inventory-to-seed-to-sale-to-GL reconciliation

- Cash controls + banking documentation

- Entity structure / related-party arrangements

- State and local indirect tax compliance

If you execute that sequence, “good in 90 days” is realistic. Not perfect, good. That means documented policies, repeatable month-end steps, and clean workpapers that tie out without heroics. It also means leadership can look at the numbers and understand what they imply for cash, taxes, and runway.

This is the core point I’ve learned working with complex operators: in cannabis, accounting isn’t bookkeeping.

It’s

risk management and decision support built to defend your tax treatment, your inventory methodology, your cash story, and your compliance record at the same time.

Frequently Asked Questions

What makes cannabis accounting different from “normal” small business accounting?

Cannabis operators face unique tax treatment (especially IRC 280E), heavier compliance expectations, and higher audit risk than most industries. Your accounting system has to separate COGS-eligible costs from non-deductible operating expenses while also supporting state reporting and seed-to-sale reconciliation.

How does IRS Section 280E change what I can deduct on my tax return?

280E generally disallows deductions for ordinary business expenses for businesses trafficking in Schedule I substances, which includes state-legal cannabis under federal law. Practically, that means your books must be clean enough to substantiate COGS and inventory capitalization, because that’s often where the biggest tax leverage exists.

Why is a strong chart of accounts (COA) so important for cannabis businesses?

A cannabis-specific COA is what allows you to consistently classify costs into production/inventory vs. selling, general, and administrative buckets that may be non-deductible under 280E. It also makes it easier to produce lender- and investor-ready reporting without rebuilding your financials every month.

What are the most common accounting mistakes that increase audit risk for cannabis companies?

The big ones are sloppy documentation, inconsistent inventory costing, commingling personal and business spend, and “creative” allocations that don’t match operational reality. Another frequent issue is failing to tie POS/seed-to-sale data to the general ledger, which creates reconciliation gaps auditors tend to focus on.

How should cannabis businesses handle cash management and internal controls?

Because many operators are cash-heavy, you need tighter controls: daily cash counts, dual custody, deposit logs, camera-supported procedures, and frequent reconciliations. Strong controls reduce shrinkage, support accurate revenue recognition, and create defensible records if you’re audited.

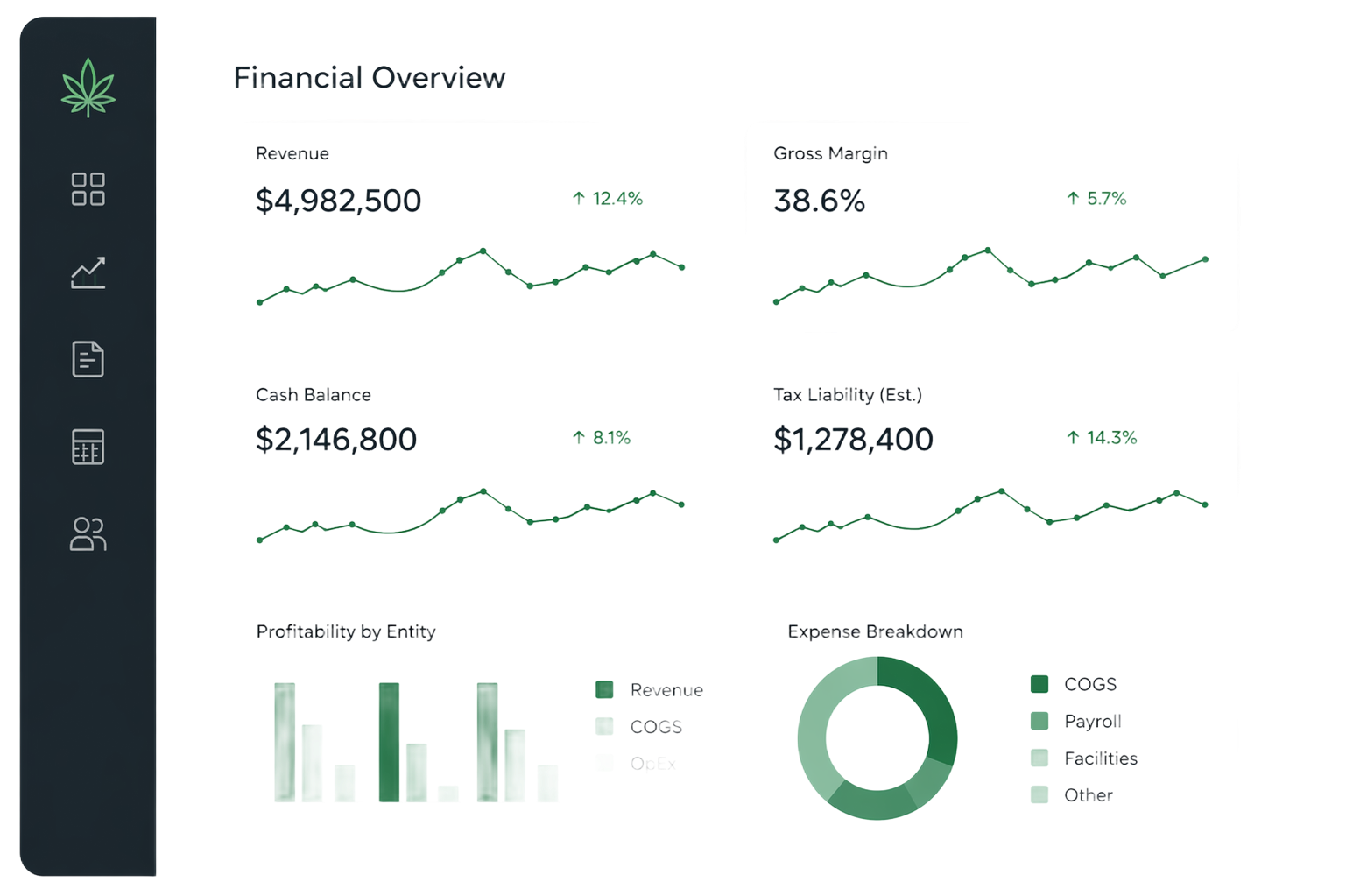

What reports should a cannabis operator review monthly to stay ahead of taxes and cash flow?

At minimum: a P&L by department/location, balance sheet, statement of cash flows (or a cash bridge), and an inventory summary that ties to POS/seed-to-sale. We also recommend a rolling cash forecast and an estimated tax view that reflects 280E impacts so you’re not surprised by quarterly payments.

Cash vs. accrual accounting—what’s better for cannabis businesses?

Many cannabis businesses benefit from accrual accounting because it improves margin visibility, supports inventory accounting, and produces more credible financials for banking, investors, and M&A. The “right” method depends on your entity, revenue model, inventory complexity, and reporting requirements—so it’s worth modeling before switching.

How do inventory and COGS affect taxes for cannabis companies under 280E?

Since many operating expenses may be non-deductible, accurate inventory costing and COGS calculation can materially impact taxable income. The key is applying consistent, well-documented costing methods and maintaining support for capitalization decisions so they’re defensible under scrutiny.

What should multi-state cannabis operators do to stay compliant with different tax rules?

Treat each state as its own compliance environment: separate tax registrations, state excise/sales tax handling, and reporting cadence—then standardize your internal processes so the data is comparable across locations. A centralized close process with location-level reporting helps you spot issues early and reduces compliance fire drills.

When should a cannabis business bring in a controller or fractional CFO?

If you’re growing locations, adding product lines, preparing for funding, or consistently surprised by taxes/cash flow, you likely need more than bookkeeping. A controller improves close accuracy and controls, while a fractional CFO builds forecasting, tax-aware planning, and decision support for expansion and profitability.

Related Blogs: