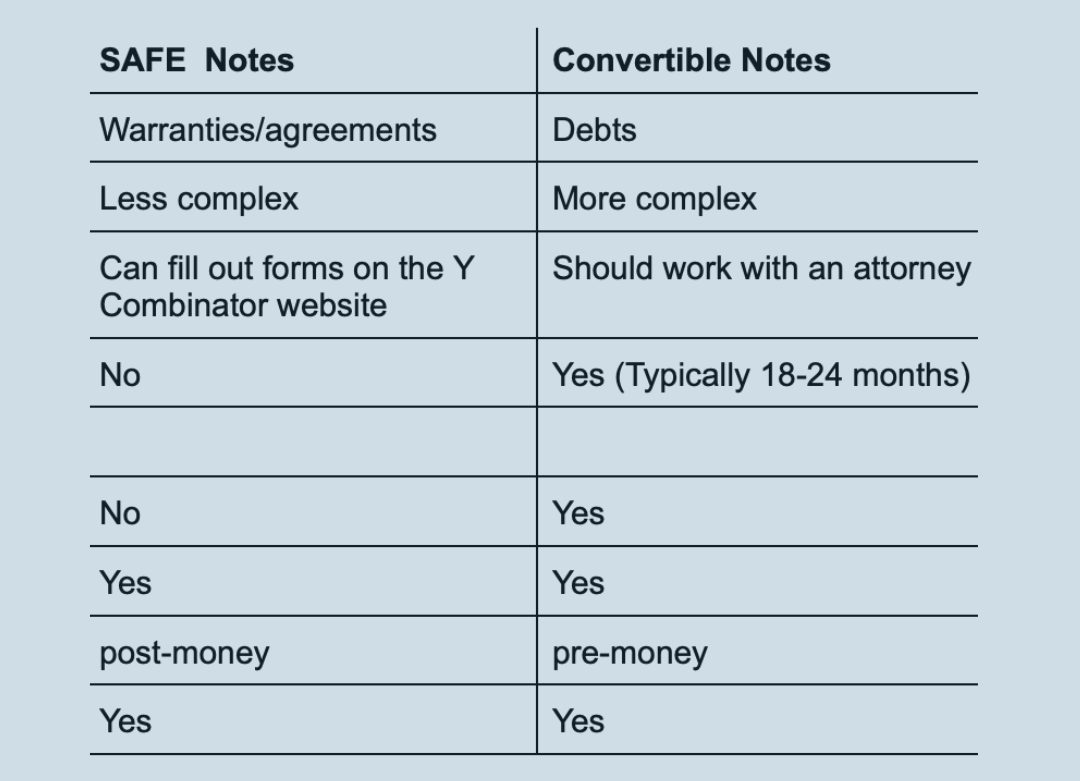

Understanding Valuation Caps

You often find Valuation Caps in Convertible Notes or SAFEs, which are commonly used in fundraising for startups.

In this article, we focus on the valuation cap of a convertible note, which is the maximum price or valuation at which the note will convert into equity.

This protects investors from dilution if the startup achieves a very high valuation in its next round, ensuring that their investment is not disproportionately small compared to the company's value. While a valuation cap doesn't prevent the company's valuation from exceeding a threshold, it limits the amount used to determine the conversion of the note to stock.

However, valuation caps can have potential drawbacks. If a startup's value grows much faster than expected in subsequent rounds, it could eclipse the cap to the investor's disadvantage. To learn more about valuation caps for SAFEs and how they play a crucial role in fundraising,

check out Y Combinator (They introduced the SAFE (a simple agreement for future equity) in late 2013.)

What Is a Convertible Note?

If you are considering convertible debt from potential investors, it is important to understand how convertible notes work. You should also consider how valuation caps can affect current shareholders, founders, and investors who buy in through the convertible note.

A convertible note is a loan that converts to equity when a triggering event occurs. (Check out TechCrunch blog)

Typically, the trigger event is when the company completes the next round of financing, also known as a priced round (or an equity investment).

Need help with your Cap Table?

Fill out the form to download our Cap Table GPT!

Here is how it works:

- An investor lends money to a startup through a convertible note.

- The loan accrues interest while it remains outstanding.

- When a triggering event occurs (typically the next funding round), the loan converts into equity.

- At conversion, the principal and accumulated interest are converted into shares based on the company’s valuation at the time of the trigger event.

This is an important factor to consider in a convertible note, as it can significantly affect the company's valuation and investors' potential returns.

Why a Floor and Convertible Note Cap?

One of the main reasons early-stage companies use convertible notes to raise capital is that the company can obtain funding without establishing a specific valuation on the business (which is needed when selling equity directly). This is particularly beneficial for early-stage companies because it gives you the chance to mature the company before determining the enterprise value at which you will sell equity. This helps to reduce dilution and raise less money, giving you a shorter runway to focus on building your business and determining the company’s current value.

A valuation cap is used in a convertible note to give the noteholders a “ceiling” value at which their investment will convert, and, in turn, that gives them a “floor” in regard to their ownership. With a valuation cap, they know their money will convert from a loan to equity at or below a per-share price determined by the issuing company's maximum valuation. This ensures that the investors are protected and have the potential to receive a higher return on their investment, as the conversion price is limited by the valuation cap.

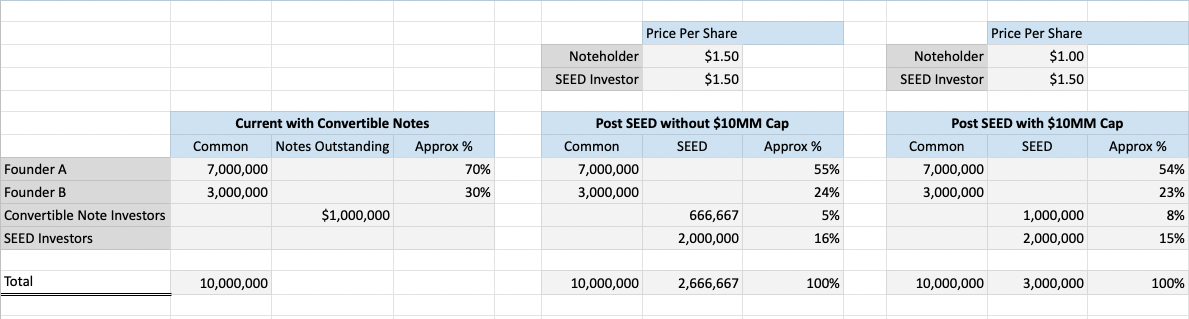

Example of a Valuation Cap

Here's a scenario with a convertible note example. Let’s say an investor invests in your company. They invest $1MM into the company via a convertible note that has a $10MM valuation cap. The cap table of the company is simple -- it has 10MM of common shares today held by two founders. Later, the company raises a Series SEED round of $3MM at a $15MM pre-money valuation, resulting in an increase in the number of shares and a potential dilution for the initial investor. This is where the terms of preferred stock, such as a valuation cap, come into play and can greatly impact the investor's return on investment.

The impact of a valuation cap on investor shares is significant:

- Scenario A: No Valuation Cap

- Conversion Price: $1.50 per share ($15MM valuation / 10MM shares)

- Shares Purchased: 666,667

- Scenario B: With $10MM Valuation Cap

- Conversion Price: $1.00 per share ($10MM cap / 10MM shares)

- Shares Purchased: 1,000,000

Investing in startups can be a complex process, but understanding terms like "valuation cap" is crucial for making informed investment decisions. On the flip side, founders need to understand the impact on their founder shares and the company. If you're still asking what is a convertible note, check out GrowthLab's Virtual CFO services and FP&A Team to help you navigate cap tables and capital raising, including the pros and cons of using convertible notes for new investors.

Benefits of Valuation Caps

You may be asking, “Why would I want to risk selling equity at a discount?” Well, you do this because many convertible note investors will require a valuation cap or discount rate in order for them to invest in the company via the note. This benefits both the company and the convertible note holder, as it allows for a lower purchase price for the shares at a subsequent equity financing. You also do this because you want to incentivize those early investors (noteholders) to bring their money in early and fast, as it can lead to potential benefits in future equity funding rounds.

Interested in Convertible Notes, SAFEs, & Caps?

At GrowthLab, we help early-stage companies like yours with cap tables,

409a, and capital raising, thoughtfully. If you’re a startup in search of investors, you can count on us to show you how to use a valuation cap to your advantage.

Key Takeaways

- Investor Protection: Valuation caps set a maximum conversion price, protecting early investors from excessive dilution during high-valuation future rounds.

- Ownership Floor: While the cap acts as a "ceiling" for the share price, it effectively creates an ownership "floor" for the noteholder.

- Founder Flexibility: Convertible notes allow startups to secure funding without immediately establishing a fixed company valuation.

- Incentivization: Caps reward early-stage investors for taking higher risks by ensuring they receive a better equity rate than later participants.

Frequently Asked Questions

Why do investors ask for valuation caps?

Investors use valuation caps to limit dilution risk. If a startup’s valuation spikes before the note converts, the cap ensures early investors aren’t disadvantaged compared to later investors who enter at a higher price.

Does a valuation cap limit how valuable my company can become?

No. A valuation cap does not cap your company’s actual valuation. It only affects the price at which the convertible note converts into equity. Your company can raise future rounds at valuations well above the cap.

How does a valuation cap affect founders?

Valuation caps can increase dilution for founders compared to a straight equity raise at a higher valuation. However, they also make early fundraising easier and faster, allowing founders to raise capital without setting a valuation too early.

What’s the difference between a valuation cap and a discount?

A valuation cap sets a maximum valuation for conversion, while a discount gives investors a percentage reduction on the share price of the next round. Some notes include both, and the investor typically converts at whichever is more favorable.

Other Blogs Related to Startup Finance